Record-high home prices have forced a shift in how buyers enter the real estate market. To afford a standard down payment, unmarried partners and platonic friends routinely pool their cash.

The financial strategy works perfectly on paper. But signing a joint mortgage without the built-in asset protection of a legal marriage leaves these buyers completely exposed. When living situations change, co-owners frequently end up deadlocked. As a result, civil courts now face a growing wave of lawsuits from buyers fighting over how to divide or sell their shared homes.

Underwood Law, a California-based partition action specialist, broke down the rise in co-ownership among unmarried couples or friends and explained the best strategies for entering into a homebuying agreement.

The Data Behind the Co-Ownership Boom

One National Association of Realtors study published earlier in 2026 sheds light on the uptick in disputes over shared ownership. While the top-level discussion in the report covers how single women now make up 25% of first-time buyers, second only to married couples, there are two other pieces of information related to unmarried couples and buyers in platonic relationships that are important to understand when looking at the modern home market.

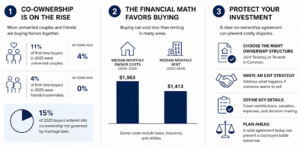

Eleven percent of the people who bought homes for the first time in 2025 were couples whoare not married, while 4% were roommates with no romantic link. Forty years ago, just 4% of first-time buyers were unmarried couples, and 0% were just friends.

This makes a total of 15% of people who entered into homebuying agreements last year doing so in a state of co-ownership not governed by the well-established legislation that comes with marriage. This is causing a legal strain, however; shared owners who fall out over a decision to sell their property are increasingly turning to partition actions to settle disputes.

Couples buying outside of wedlock and friends investing in property to share often do not realize that costly court proceedings can result when a disagreement arises. It is generally advisable to seek mediation before going any further, although knowing that a partition action may be used to force a sale of the property in the event of a shared-ownership impasse is reassuring.

The Financial Math of Buying Over Renting

Despite the growing threat of courtroom disputes, the incentive for unmarried buyers to bypass the rental market comes down to basic math.

Data from the U.S. Census Bureau shows that 20% of counties saw rent increases between 2020 and 2024, with a median monthly payment of $1,413. Given that the same dataset showed median household costs for owner-occupied properties were static at $1,963 over the same period, the upsides of buying over renting are obvious. The figure for homeowners includes other associated costs, such as taxes and utility payments, while the rental figure does not.

In other words, there’s a strong incentive for couples and friendship groups to pool their resources and buy a place if that’s an option. Renting feels like spending money without seeing any return on that capital, but rushing into shared homes has its own repercussions.

Drafting a Co-Ownership Exit Strategy

Owners of shared homes, whether unmarried couples or cohabiting platonic companions, must ensure they establish the rules and expectations for this arrangement as part of the purchase process. While demanding a formal contract with a romantic partner or close friend may seem transactional, relationship dynamics and financial priorities inevitably shift over time. Having a formal shared ownership agreement in place, ideally drafted and overseen by a legal professional, makes a later partition action far less likely.

To do this effectively, buyers must first determine how they will hold the property title. Structuring the purchase as a "Joint Tenancy" grants both partners an equal share with the right of survivorship, meaning the property automatically transfers to the surviving owner if one passes away. Conversely, "Tenants in Common" allows for unequal ownership splits—such as a 70/30 division based on down payment contributions—but lacks survivorship rights, meaning a deceased partner's share passes to their designated heirs rather than the co-owner.

The specifics of the agreement can vary, but the general contents will cover aspects such as what happens if one party wants to sell but the other doesn’t, and how that sale would be handled, including everything down to the property's valuation.

Committing to an agreement when buying shared homes together with a partner or friend is a logical response to the reality of rising disputes and partition actions. As macroeconomic conditions push more buyers into shared mortgages, implementing a proactive legal framework ensures that a strategic financial decision today does not turn into a drawn-out courtroom dispute tomorrow.