For unmarried partners and cohabiting couples navigating a highly inflated housing market, pooling financial resources is increasingly the only viable path onto the property ladder. Data from the National Association of Realtors (NAR) indicates their stake among first-time buyers has jumped from 4% in 1985 to 11% in 2025. However, while joint mortgages solve an immediate economic problem, standard property laws are falling behind these shifting relationship dynamics. Underwood Law examines what co-owners should know to avoid ending up in court upon discovering one person wants to sell but the other disagrees.

A Matter of Economic Inevitability

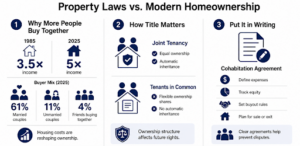

The latest NAR data on the U.S. market’s first-time buyers in 2025 highlights the macroeconomic shifts dictating how people get onto the property ladder today. Couples, both married and unmarried, still make up the lion’s share at 61%, and the rise of cohabiting couples who’ve not yet tied the knot but share a mortgage has a simple economic explanation.

In 1985, the year of comparison used in the report, the median household income was $23,620, and the median sales price for a home was $82,800, meaning a typical property cost roughly 3.5 times a buyer's annual salary. When adjusted for inflation, that $82,800 is equivalent to approximately $228,500 in today's dollars.

By contrast, looking at what a median-priced home actually cost in 2025, the figure is roughly $416,900, showing that housing costs have drastically outpaced general inflation. That’s equivalent to 5 times the median household income.

Then there’s the pressure exerted by the cost of getting married. The average cost of a 2025 wedding according to The Knot was about $34,000.

Couples are squeezed at both ends. Buying a home is more expensive and rents are rising year on year, so there’s more of an incentive to buy a home together rather than hold out until after a marriage. For a typical wedding’s budget, couples can have a significant part of a mortgage down payment, so for a lot of couples, the most financially prudent choice is to make buying a home a priority.

This also explains why 4% of first-time buyers in 2025 were not couples at all, but rather groups of friends choosing to prioritize property ownership. There are economic benefits to this model, but the long-term implications for property laws are less well understood by average buyers.

A Legal Conundrum

What couples overlook, and what the legal system is having to contend with, is that co-owning a property as an unmarried couple brings a range of complications and concerns along with it.

When an unmarried couple buys a home, how they hold the title matters just as much as whose name is on the mortgage. Generally, they have to choose between two main legal structures, and each handles the future very differently.

Protecting Equity with Joint Tenancy

Both partners own an equal 100% share of the property. The defining feature here is the right of survivorship, and if one partner passes away, their share automatically transfers to the surviving partner, bypassing wills and probate entirely.

The Inheritance Risks of Tenants in Common

Ownership doesn't have to be equal. If one partner contributes 70% of the down payment and the other puts in 30%, the title can reflect that exact split. However, there is no right of survivorship. If one partner dies, their share goes to whoever is named in their will, or their next of kin, which can leave the surviving partner owning a house with their late partner’s family.

Considering Cohabitation Agreements

To mitigate these title risks, a growing number of real estate professionals advise executing a formal Cohabitation Agreement or Property Ownership Agreement concurrently with the mortgage signing.

A comprehensive agreement explicitly outlines recurring financial liabilities—detailing who is responsible for the mortgage payments, property taxes, insurance, and maintenance fees—and explicitly defines how those contributions alter ownership equity over time. Crucially, the document serves as an operational exit strategy.

It dictates structural procedures if the relationship ends, determining whether one partner retains the right of first refusal to buy out the other's equity, how the home will be appraised, and the exact timeline required before the property must be placed on the open market.

Property Laws, Homeownership, and Marriage Trends in an Uneasy Alliance

Choosing to buy a home before or instead of getting married is a highly pragmatic response to a brutal 2026 housing market and broader economic realities. Pooling resources is often the only viable way onto the property ladder.

However, bypassing the altar shouldn't mean bypassing the paperwork. Taking the time to establish a clear, legally binding framework at the start ensures that a smart financial move today doesn't turn into a costly legal battle tomorrow.